|

This year, Sleep Review partnered with Wachovia Capital Markets LLC to conduct our annual salary survey and Q3 market survey of sleep centers. Survey data was compiled from responses that were received from 772 sleep laboratories between June 23 and July 1, 2008. Results of Wachovia’s Q1 Sleep Center Survey indicated that sleep labs were limiting their expansion plans given Medicare’s proposal to cover home testing for obstructive sleep apnea (OSA). In fact, in the report (released February 12, 2008), 40% of the respondents indicated that home testing had affected their expansion plans. Now, results of the Sleep Review/Wachovia Q3 Sleep Center Survey indicate that sleep lab expansion is expected to stabilize as concern about the impact of home sleep testing is fading.

Download complete results of the Q3 2008 Sleep Center Survey. |

CONDUCTING THE SURVEYFor the first time, Sleep Review partnered with equity research firm, Wachovia Capital Markets LLC. Among the roughly 12,500 sleep professionals to whom we sent the survey, 772 responded to one or more of the survey questions for a response rate of 6%. Because none of the questions in this survey were mandatory, the response rates varied from question to question. We received responses from a range of sleep industry participants with registered polysomnographic technicians (37% of respondents) and sleep center directors/supervisors/managers (29% of respondents) representing the most common titles. Responses also covered every geographic region (and nearly every state) in the United States. |

SURVEY SAYS … |

|

|

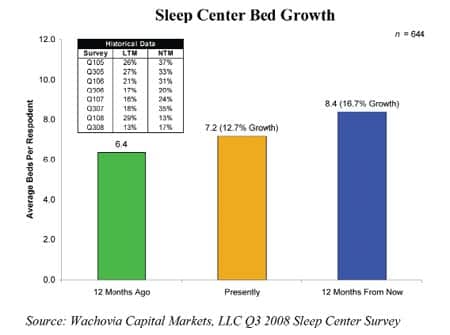

Sleep center expansion slowed over the past year but looks likely to stabilize over the next year.

Bed Growth During Prior 12 Months: Respondents saw bed growth of 13% during the past 12 months and reported an average of 7.2 beds per respondent versus 6.4 beds per respondent 12 months ago. We should note that sleep center growth covers only part of the entire sleep market, as sleep center growth drives new diagnoses and flow generator sales, while mask sales are mostly driven by replacement sales. Moreover, sleep center growth as defined in the survey only represents organic growth (beds per center) versus inorganic growth (new sleep centers). That being said, the survey demonstrates a decrease in bed growth to a level in the low teens range. The sharp slowdown in sleep laboratory expansion may have been driven by the prospect of home sleep testing. Medicare proposed coverage of home testing in December 2007 and then finalized coverage in March 2008. Given the uncertain repercussions posed by the coverage decision, it is not surprising that sleep laboratories may have slowed expansion around this time. The survey indicates that flow generators (driven mainly by new patients) have been growing at 8% to 10%, while masks (driven by both new patients and increasing replacement among existing patients) have grown at 13% to 15%; combined, this puts the market in the low teens. Expected Bed Growth During Next 12 Months: Respondents expect faster sleep center capacity expansion in the next 12 months (17% to 8.4 beds per respondent) than the growth seen in the past 12 months. However, prior surveys indicate that sleep centers tend to overestimate their projected growth rates by 150% to 200%. Therefore, sleep center growth is likely to be stable in the low teens over the next 12 months. Why the stabilization? Analysts believe that the sleep centers’ initial fears of home testing may be easing because reimbursement is likely to be less than expected and because CMS has restricted home medical equipment providers from administering tests. |

PORTABLE MONITORING IN SLEEP CENTERS SLOW GOING |

||||||||||||||||||

On the home testing front, respondents indicated that home testing would most likely get a lukewarm reception at sleep centers. Currently, just 13% of the sleep centers offer home sleep tests. In the next 6 months, another 33% expect to start offering home sleep tests. However, when asked about what level of reimbursement it would take for the sleep centers to adopt home testing, the average response was $428 per test. That figure is far from G-code reimbursement rates released by carriers such as HealthNow New York Inc, doing business as Blue Shield of Western New York. Those rates are:

These payment rates are below the $428 rate it would take for the average, surveyed lab to adopt home testing. Consequently, adoption of home testing by sleep centers may be limited. Supporting the thesis that the uncertainty created by home testing coverage has slowed sleep laboratory expansion and growth expectations is the fact that 23% of sleep laboratories surveyed indicated that the potential for increased use of home diagnosis has affected their expansion plans. The sleep centers expect to make only moderate changes to their practices in the face of increased use of home testing. Approximately 38% of respondents say that they would increase involvement with home testing, while only 2% would reduce the number of beds at their facilities, 1% would close facilities, and 27% expect to make no changes.

|

MORE PATIENT VOLUME EXPECTED |

|

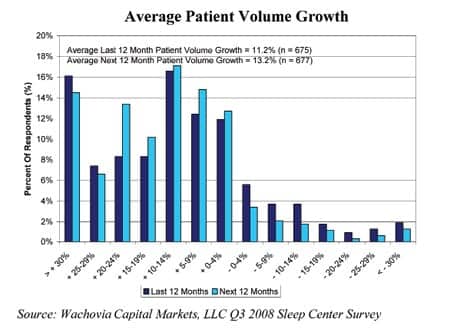

Respondents reported that overall, sleep centers have seen patient volume grow by 11% in the past 12 months and expect 13% growth in the next 12 months; the most common response for both was 10% to 14% growth.. These numbers are slightly behind both the reported and expected bed growth rates (which were 13% and 17%, respectively). Wachovia analysts are not sure how to explain the discrepancy between these two questions; however, one possible explanation might be that there is a lag between sleep center expansion and patient volume growth. It is only the third time that our survey partner, Wachovia, has asked this particular question about future growth, so it is a bit early to evaluate longer term trends in patient volume. Last 12 months growth in this survey was down slightly from Wachovia’s prior two surveys (10% versus 13% and 13%) though next 12 months growth in this survey was between their prior two surveys (13% versus 17% and 10%). |

SELLING SLEEP THERAPY EQUIPMENT |

|

The survey shows a gradual increase in sleep laboratories selling sleep therapy equipment from 16% of laboratories in a Wachovia Q1 2006 survey to 19% in the Q3 2008 survey. Some laboratories have started to view equipment as an additional revenue source and a way to offset potential losses to home sleep testing. However, this revenue model might be challenged (at least for Medicare patients) given a proposal from CMS to disallow CPAP sales by companies administering tests and vice versa. This CMS proposal is not final, however. It should be noted that information in this report has been obtained or derived from sources believed by Sleep Review to be reliable. Any opinions or estimates contained in this report represent the judgment of Sleep Review and Wachovia Capital Markets LLC at this time, and are subject to change without notice. We advise readers to compare our results to other surveys.To view the full breakdown of the number of our regional responses, view the complete results here. |

{kind=link}