|

Narrowing in on the impact of the economy on the sleep industry, data from the Wachovia/Sleep Review Q1 2009 Sleep Center Survey revealed that the credit crunch is taking a toll on sleep centers. Nearly half of survey respondents reported a negative impact on patient volumes and slightly less reporting delayed expansion plans.

THE BIG PICTURE: SLEEP LABORATORY EXPANSION SLOWINGSleep centers in the survey report expanding bed capacity by 5% in the last 12 months (LTM), down from 13% from our Q3 2008 survey. The centers reported that they plan to expand beds by 13% in the next 12 months (NTM), which is down from 17% in our Q3 2008 survey. Similarly, the sleep centers report that patient volumes were up 7% in the LTM (down from 11% in the Q3 2008 survey) but are expected to be up 10% in the NTM (down from 13% in the Q3 2008 survey). Based on this, the CPAP market is projected to grow by 10% to 12% during 2009 with 7% to 8% patient growth and 3% to 4% growth from increased mask replacement rates as home medical equipment companies (HMEs) maximize recurring revenue to offset reimbursement cuts.

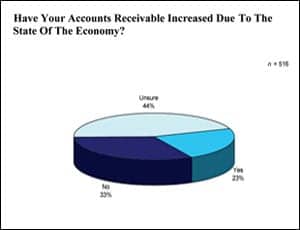

Meanwhile, the economy and credit crunch are taking a toll on sleep centers. When asked about the impact of the economy, 47% of respondents reported a negative impact on patient volumes, and 40% indicated that the economy, credit crunch, or both had caused expansion plans to be delayed. Specifically, 18% of our respondents report more difficulty in obtaining loans or raising debt financing, and 5% of respondents report paying higher interest rates. Only 23% of respondents have seen accounts receivable increase due to the economy. |

SLEEP CENTER PATIENT VOLUME STILL GROWING, BUT SLOWEROn average, respondents have seen patient volume grow 7% in the LTM and expect 10% growth in the NTM. While the above figures still show growth, it should be noted that the LTM and NTM growths in the current survey were both down from prior surveys.

Two potential reasons that patient volumes are slowing are: First, the sleep market is maturing and penetration is increasing (ie, the “law of large numbers”), and second, the economy entered a recession in late 2007, which intensified during 2008. If the economy is a factor in the slowdown, growth rates should improve as economic growth rebounds. |

ECONOMY MODESTLY IMPACTING SLEEP CENTERSPrevious surveys had not focused on the economy. However, given the state of the US economy and investor concerns over the economy’s impact on the sleep apnea market and the broader health care industry, this survey added several questions on this topic. About half (47%) of the respondents indicated that the economy has had a negative impact on patient volumes.

According to Wachovia analysts, the “electiveness” of sleep apnea treatment is largely a function of the severity of the disease. Patients with severe sleep apnea are unlikely to view treatment as elective given how great an impact CPAP therapy has on their quality of life. These patients are a minority, however. The far larger segment of the sleep market is patients with moderate or mild sleep apnea. While these patients’ health benefits greatly from CPAP therapy, the short-term benefits are less clear. As a result, this portion of the market is most likely highly elective with substantial economic sensitivity. It is also noted that while CPAP therapy is nearly universally covered by Medicare and insurers, patients may have to pay significant deductibles or co-payments “out-of-pocket.” Given the economic sensitivity reported by the sleep laboratories, it is not surprising that 40% of the laboratories have delayed expansion plans as a result of the economy and/or the credit crunch.

|

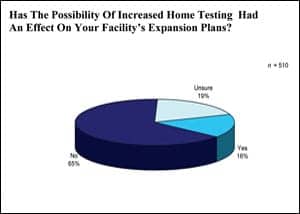

FEW SLEEP CENTERS ADMINISTERING HOME TESTING FOR NOWCurrently, only 14% of sleep laboratories administer home OSA testing. However, another 25% responded that they are likely to start to administer home OSA tests in the next 6 months. It is possible that the threat of home testing has moderated some in the eyes of sleep laboratories with only 16% of sleep laboratories surveyed indicating that the potential for increased use of home diagnosis has affected their expansion plan. This response is down substantially from the 40% reported in our Q1 2008 survey.

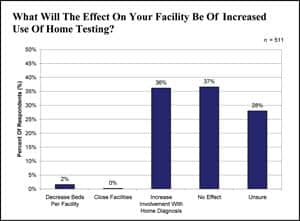

The sleep centers surveyed expect to make only moderate changes to their practices in the face of increased use of home testing. Around 36% of respondents would increase involvement with home testing, while only 2% would reduce the number of beds at their facilities. Less than 1% of respondents report that they would close facilities, and 37% expect to make no changes. These numbers were down significantly from the Q1 2008 survey, in which 15% of respondents expected to reduce the number of beds at their facilities and 5% of respondents expected to close facilities. Sleep centers were also asked about their expectations regarding reimbursement for home sleep tests. On average, the sleep centers indicated that they would need $420 per home test to begin home testing. This is well above the level that Medicare intends to pay (around $150). As a result, adoption of home testing may be inhibited due to a lack of financial incentive. Responses also indicated a slight increase in sleep laboratories selling CPAP equipment from 16% of laboratories in the Q1 2006 survey to 19% in the Q1 2009 survey. It is possible that some laboratories view equipment as an additional revenue source and a way to offset potential losses to home sleep testing.

|

ABOUT THE SURVEY

The survey was sent to 12,500 sleep professionals. There were 560 who responded to one or more of the survey questions for a response rate of 5%. Responses were received from a range of sleep industry participants. Sleep center directors, supervisors, and managers (32% of respondents) and registered polysomnography technicians (30% of respondents) represented the most common titles.

Responses also covered every geographic region and 48 of the 50 states. The Midwest (31% of respondents) and Southeast (28% of respondents) are the most heavily represented of the respondents.

Sleep Review would like to thank our survey partners at Wachovia and all in the sleep community who participated in these surveys.

{kind=link}